-

-

Published on

22/04/2016

by Punchmedia

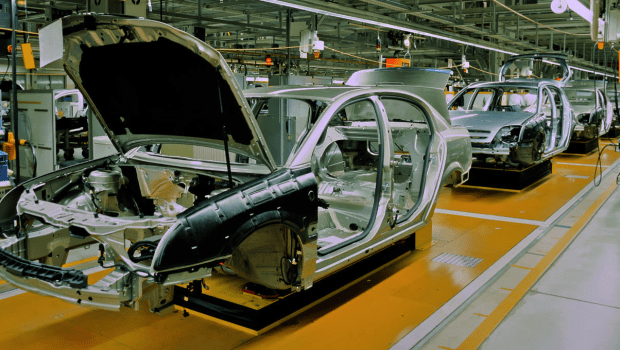

Automotive Growth Despite Offshore Push

The Automotive industry encompasses each level of the passenger vehicle supply chain, from manufacturing through to wholesaling and retailing. The industry also includes repair and maintenance operators. Local manufacturers have struggled over the past five years due to the high Australian dollar for much of the period, reduced import protections and consumers' shifting preference towards smaller fuel-efficient imported cars. These trends have not been detrimental to all segments of the industry, as sales growth for imported vehicles has enabled wholesalers and some dealers to offset much of the decline from manufacturers. Industry revenue is forecast to grow at a compound annual rate of 1.1% over the five years through 2015-16, to reach $161.9 billion. The industry's steady growth follows a significant decline at the beginning of the period, largely due to the Japanese tsunami in March 2011. The tsunami disrupted the automotive supply chain for parts and vehicles imported from Japan, one of the main motor vehicle importers to Australia. In the current year, industry revenue is forecast to grow by 1.7%, due to a projected rise in consumer sentiment alongside the implementation of free trade agreements with Japan and Korea, which have begun to reduce the cost of imported vehicles from these countries.

Participation and profit

All entities within each automotive-related industry contribute towards the Automotive industry's overall revenue. While this can result in double-counting due to the high value of purchases by dealers from other motor vehicle manufacturing and wholesaling entities, it reflects the sum of each establishment's revenue. The number of establishments has fallen slightly over the past five years as many parts manufacturers have been forced to close. However, growth in demand for repair and maintenance services, along with sustained high demand for new cars, has resulted in a slight uptick in industry employment. Over the past five years, manufacturers have had to cut highly paid engineering workers and have been unable to provide more working hours to production line employees. However, this has been offset by dealership sales staff earning higher commissions, which has helped drive growth in the average industry wage. Industry profit margins have fallen over the past five years, caused by the reduced economies of scale and pending manufacturing exits of local motor vehicle manufacturers. Strong price competition at the wholesale and retail levels of the automotive supply chain has prevented the growing demand for new motor vehicles from boosting margins.Breaking It Down

New passenger vehicle sales have grown strongly over the past five years, primarily due to the largely positive consumer sentiment and growth in disposable income over the period. However, the strength of new car sales has not extended to locally manufactured vehicles. Local motor vehicle manufacturers Toyota, GM Holden and Ford have all struggled as consumers have increasingly opted to purchase imported fuel-efficient vehicles. Sales of these vehicles benefited from the high Australian dollar for much of the period, as well as the reduction in the motor vehicle tariff in 2010 and free trade agreements with Japan and Korea. Despite heavy government subsidisation, these conditions have caused large drops in revenue and profitability for the manufacturing operations of the major players. Toyota, GM Holden and Ford have all announced their intention to exit manufacturing operations over the next five years, to become solely importers. Weaker demand for locally manufactured motor vehicles has also travelled upstream in the supply chain to parts manufacturers. While motor vehicle dealers have been able to obtain imported vehicles from wholesalers, upstream parts manufacturers have traditionally relied on local motor vehicle manufacturers for supply contracts. As the demand flowing upstream has dried up, parts manufacturers have lowered their production volumes, which has increased per-unit costs. The resulting disadvantage in economies of scale compared with parts and accessories importers has forced many local parts manufacturers into administration over the past five years.Import Growth

The severe decline in manufacturing over the past five years has been largely due to increasing import penetration. The high cost of fuel early in the period encouraged consumers to purchase smaller fuel-efficient cars. These vehicles are typically cheaper than the large cars traditionally produced by Australian manufacturers, reducing the price paid per vehicle sold. However, revenue increases from the strong demand growth have outstripped the revenue losses caused by selling cheaper vehicles, particularly for importing wholesalers. Strong import growth is evident in the strong sales performance of imported small cars such as the Mazda3, which ended the Holden Commodore's 15-year reign as the top-selling new car in Australia in 2011. The Mazda3 and other small cars, like the Toyota Corolla, have continued to perform strongly in terms of sales volumes. The high Australian dollar made imported vehicles comparatively cheaper in the domestic market, as did the tariff reduction on imported vehicles from 10.0% to 5.0% in January 2010. In addition, overseas manufacturers in lower cost countries like Thailand tend to have significantly lower wage costs, whereas cars manufacturers in large developed countries like Japan and Germany benefit from much greater economies of scale. While the low price of imports has been to the ultimate detriment of local automotive manufacturing industries, it has made imported vehicles highly attractive to consumers. Wholesalers and dealers have been the primary beneficiaries of this growth in demand.Repair and Maintenance

Demand for repair and maintenance industries has grown steadily over the past five years. While strong new car sales have softened the demand for repair work performed by mechanics and auto electricians, demand for vehicle servicing has grown as many new cars have included servicing and maintenance for a specific time frame. Purchasers of new vehicles have also increasingly bought vehicle add-ons, which has benefited parts wholesalers and parts retailers. Furthermore, despite the increased safety features and reliability afforded by new vehicles, demand for smash repairers has remained fairly stable as a higher number of vehicles on the road typically leads to a greater volume of vehicle accidents.

Related articles

-

06/02/2014 by Melinda.OliverAustralian consumers spent $14.7 billion on online retail in the year to December 2013, with momentum up in the last month of the year, according to the NAB Online Retail Sales ... Read more

06/02/2014 by Melinda.OliverAustralian consumers spent $14.7 billion on online retail in the year to December 2013, with momentum up in the last month of the year, according to the NAB Online Retail Sales ... Read more -

25/02/2014 by gavinLowerAustralian small businesses are feeling positive about their current and future performance, according to the first Westpac-Melbourne Institute Small Business Index. The index,... Read more

25/02/2014 by gavinLowerAustralian small businesses are feeling positive about their current and future performance, according to the first Westpac-Melbourne Institute Small Business Index. The index,... Read more -

25/02/2014 by Alexandra CainA once-in-a lifetime opportunity to make a fortune is there for the taking. But it won't last long. There are thousands of small businesses on the market at bargain basement pr... Read more

25/02/2014 by Alexandra CainA once-in-a lifetime opportunity to make a fortune is there for the taking. But it won't last long. There are thousands of small businesses on the market at bargain basement pr... Read more